Role of Blockchain in Cross-Border Payments: A Complete Guide

Cross border payments stand as one of the most complicated elements of international finance. Intermediary networks, high processing fees, currency conversion inefficiencies, and fragmented regulatory frameworks still hinder international transactions despite the fast progress of digital banking. Companies that operate in multiple regions experience payment delays and a lack of visibility, and unpredictable expenses, which result in cash flow problems and difficulties with their operational schedules.

The current pace of global business is outpacing the existing payment infrastructure, which is struggling to keep up with the requirements of speed, transparency, and cost-effectiveness. Blockchain technology in cross border payments is changing this paradigm. Blockchain technology eliminates the need for complex middleman correspondent banking networks by using distributed ledgers, which provide real-time settlement, transparent transactions, and less reliance on middlemen.

From our experience in blockchain development, we have seen how distributed ledger technology can address long-standing inefficiencies in international payment systems. Enterprises are no longer exploring blockchain as an experimental technology. They are implementing it as a strategic infrastructure upgrade to improve liquidity management, reduce operational risk, and unlock new global revenue streams.

This blog examines the current challenges in cross border payments, the transformative role of blockchain, and the strategic considerations businesses must evaluate when building or adopting blockchain-based payment solutions.

- Blockchain in cross border payments reduces settlement time, costs, and reliance on intermediaries.

- Traditional international payment systems face delays, liquidity constraints, and regulatory fragmentation.

- Enterprises are adopting blockchain to improve transparency, automate workflows, and unlock new revenue models.

- Regulatory alignment, secure infrastructure, and strategic partnerships are critical for successful implementation.

- Cross border payment systems are constrained by correspondent banking layers, high foreign exchange spreads, limited transparency, and complex compliance requirements across jurisdictions.

- Blockchain in cross border payments enables near real-time settlement, immutable transaction records, and automated execution through smart contracts, significantly improving operational efficiency.

- Stablecoins and tokenized fiat are accelerating adoption by offering predictable value transfer mechanisms for both B2B and B2C international transactions.

- Businesses can monetize blockchain-based payment platforms through transaction fees, FX optimization, liquidity services, and API driven financial integrations.

- A scalable solution requires the right blockchain architecture, embedded compliance controls, secure wallet infrastructure, and seamless integration with banking systems.

- Global regulatory frameworks across North America, Europe, Asia Pacific, and the Middle East are evolving rapidly, making compliance readiness a foundational requirement.

- Organizations that strategically implement blockchain in cross border payments gain improved liquidity management, reduced operational risk, and a stronger competitive position in global commerce.

The Current Challenges in Cross Border Payment Systems

Cross border payments form the backbone of global trade, yet the infrastructure supporting them remains fragmented and inefficient. Traditional systems were not designed for today’s real-time, digital economy. As transaction volumes grow and markets expand, the limitations of legacy frameworks become more visible.

Below are the key challenges businesses continue to face:

- Multiple Intermediaries and Delays: International transfers typically pass through correspondent banks and clearing networks before reaching the beneficiary. Each intermediary adds processing time, operational complexity, and additional fees. Settlements can take several days, particularly when multiple currencies are involved.

- High Transaction and FX Costs: Cross border payments often involve layered charges, including service fees, currency conversion spreads, and intermediary bank costs. For businesses processing large volumes, these cumulative expenses significantly impact margins.

- Limited Transparency and Traceability: Tracking international transactions across multiple banking systems is difficult. Payment status visibility is often delayed, creating uncertainty for both senders and recipients. This lack of transparency affects financial planning and supplier relationships.

- Regulatory Fragmentation: Each jurisdiction maintains its own compliance standards, reporting requirements, and anti-money laundering frameworks. Navigating these regulations increases operational burden and compliance costs for financial institutions and enterprises.

- Liquidity Management Challenges: Financial institutions must maintain pre-funded accounts across different countries to facilitate settlements. This locks up capital and reduces operational efficiency.

- Settlement Risks and Errors: Manual processes, time zone differences, and inconsistent data standards increase the risk of errors and payment failures. Resolving disputes can be time-consuming and expensive.

These persistent inefficiencies are driving interest in blockchain in cross border payments. Businesses are seeking infrastructure that delivers faster settlement, greater transparency, and cost efficiency without relying on outdated correspondent banking networks. In the next section, we explore how blockchain technology directly addresses these structural challenges.

Also Check: Top Cold Crypto Wallets: Ultimate Security Guide

How Blockchain in Cross Border Payments Is Transforming Global Transactions

Blockchain technology is redefining how money moves across borders. Traditional systems remain slow, opaque, and costly. Businesses and individuals are pushing for alternatives that deliver near real-time settlement, lower fees, and clear audit trails. Blockchain in cross border payments is emerging from niche experimentation into practical deployment across both business-to-business and consumer contexts.

The global cross border payments market continues to expand. Total flows are projected to reach nearly $290 trillion by 2030 as digital commerce and international trade grow rapidly. Blockchain-based mechanisms are starting to capture a meaningful share of this volume as enterprises and payment providers integrate digital assets into their payment rails.

- Stablecoins, which operate on blockchain networks, illustrate this shift. In 2025, the total stablecoin transaction volume climbed into the tens of trillions of dollars, with annual payment volume hitting levels far above prior years. Active usage of stablecoins grew more than 140 percent year over year on major platforms, while overall transaction activity surged by more than 200 percent, showing that blockchain-based transfers are moving beyond pilot projects into real commerce use.

- Businesses are responding to these trends. A recent industry survey found that nearly two-thirds of companies already use stablecoins for cross border payments or plan to adopt them within a few years. Speed, predictable costs, and the ability to settle transactions without pre-funded correspondent accounts are primary drivers of this shift.

The impact spans multiple use cases. For B2B transactions, blockchain enables reconciliation of complex supplier payments with clear time stamping and fraud-resistant records. For B2C and C2B flows, blockchain-based transfers reduce reliance on legacy networks that often charge high fees for remittances and consumer payouts. Industry forecasts suggest that digital assets could account for 5 to 10 percent of total cross border payments by 2030, which translates into trillions in transaction value settled on blockchain rails.

The momentum of blockchain in cross border payments signals a shift from traditional banking corridors toward a distributed infrastructure that supports faster settlement, increased transparency, and predictable cost structures. As adoption grows, these technologies will shape the future of international commerce and financial connectivity.

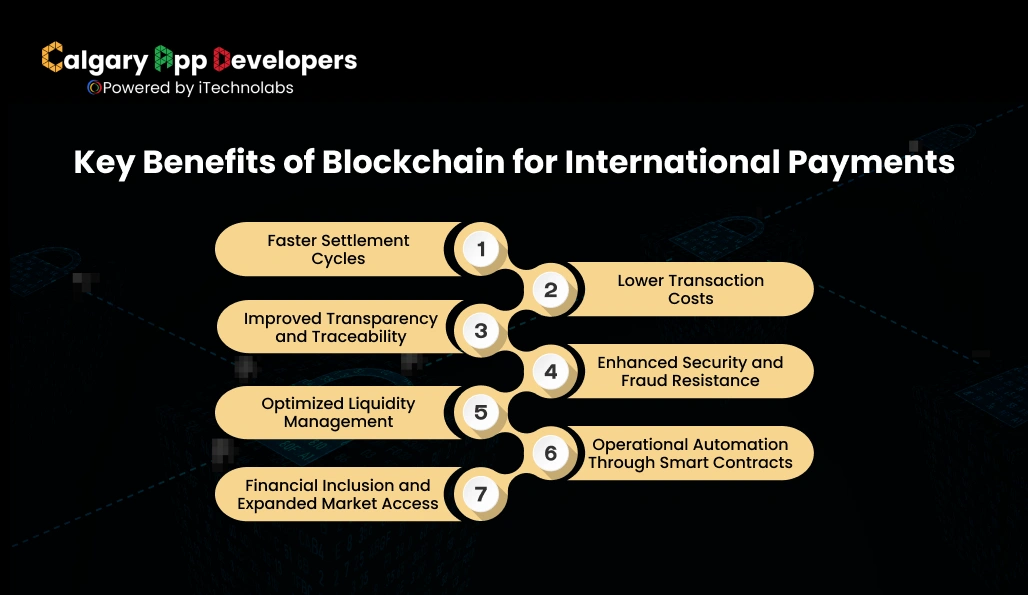

Key Benefits of Blockchain for International Payments

The growing adoption of blockchain in cross border payments is driven by measurable operational and financial advantages. Organizations are no longer evaluating blockchain as a theoretical innovation. They are implementing it to solve real settlement, liquidity, and transparency challenges that traditional systems have failed to address.

Below are the core benefits reshaping international payment infrastructure.

- Faster Settlement Cycles:

Blockchain enables near-real-time transaction validation and settlement. Instead of waiting several business days for correspondent banking processes to clear, transactions can be confirmed within minutes. This acceleration improves working capital efficiency and strengthens supplier relationships.

- Lower Transaction Costs:

By reducing reliance on intermediary banks and clearing networks, blockchain significantly decreases processing fees. Currency conversion can be executed through digital assets or tokenized fiat mechanisms, lowering foreign exchange spreads and eliminating layered charges.

- Improved Transparency and Traceability:

Distributed ledger technology records transactions on a shared, tamper-resistant ledger. Each participant can verify payment status in real time. This visibility reduces disputes, simplifies reconciliation, and enhances audit readiness.

- Enhanced Security and Fraud Resistance:

Cryptographic validation and decentralized consensus mechanisms make unauthorized alterations extremely difficult. The immutability of blockchain records strengthens transaction integrity and reduces fraud exposure.

- Optimized Liquidity Management:

Traditional cross border payments often require pre-funded accounts across multiple jurisdictions. Blockchain-based systems allow on-demand liquidity models, minimizing capital lockup and improving balance sheet efficiency.

- Operational Automation Through Smart Contracts:

Smart contracts can automate conditional payments, compliance checks, and settlement triggers. This reduces manual intervention, lowers error rates, and increases processing efficiency.

- Financial Inclusion and Expanded Market Access:

Blockchain networks can connect institutions and businesses in regions with limited traditional banking infrastructure. This expands access to global trade and creates new revenue opportunities in emerging markets.

The adoption of blockchain in cross border payments is not simply about speed. It represents a structural shift toward more transparent, cost-efficient, and scalable financial networks capable of supporting the next phase of global commerce.

Also Read: Blockchain Wallet Development: An Ultimate Guide

What This Means for Businesses: Market Potential and Revenue Opportunities

The expansion of blockchain in cross border payments represents a significant commercial opportunity for financial institutions, fintech companies, and global enterprises. As international trade volumes continue to rise and digital commerce expands across emerging markets, demand for faster and more cost-efficient payment infrastructure is accelerating. Businesses that integrate blockchain-based settlement mechanisms can reduce operational costs while unlocking new revenue streams tied to transaction processing, liquidity services, and digital asset management.

For fintech platforms, blockchain enables the creation of value-added services such as real-time FX conversion, programmable escrow, and cross border treasury optimization. Banks can modernize legacy systems while retaining regulatory control and improving customer experience. Enterprises operating globally gain greater predictability in settlement timelines and cost structures, improving cash flow forecasting and capital allocation strategies.

As adoption grows across B2B and B2C ecosystems, blockchain in cross border payments is evolving into a scalable infrastructure layer that supports both efficiency gains and long-term revenue diversification.

Essential Features of Blockchain-Based Cross Border Payment Solutions

A successful platform built around blockchain in cross border payments must go beyond basic transaction processing. It should combine technical efficiency, regulatory readiness, and enterprise-grade security to support high-volume international flows. The following features are critical to building a scalable and commercially viable solution.

- Multi-Currency and Multi-Asset Support: The system should support fiat currencies, stablecoins, and tokenized assets to enable flexible settlement options across jurisdictions.

- Real Time Settlement and Transaction Finality: Near real-time validation ensures faster fund transfers and reduces counterparty risk. Clear transaction finality is essential for enterprise confidence.

- Integrated Compliance and KYC Modules: Built-in identity verification, AML screening, and transaction monitoring tools help ensure adherence to global regulatory requirements.

- Liquidity Management Mechanisms: On-demand liquidity models and smart routing capabilities reduce reliance on pre-funded accounts and optimize capital efficiency.

- Smart Contract Automation: Automated execution of conditional payments, escrow arrangements, and reconciliation processes increases operational efficiency and minimizes manual errors.

- Enterprise Grade Security Framework: Encryption, multi-signature authentication, and secure key management are essential for safeguarding digital assets and transaction data.

- Interoperability with Banking and Payment Networks: Seamless API integration with existing financial systems ensures smooth adoption without disrupting core operations.

- Scalable Infrastructure Architecture: The platform should handle increasing transaction volumes while maintaining speed, stability, and performance across global markets.

These features collectively define a resilient infrastructure capable of supporting modern international commerce powered by blockchain in cross border payments.

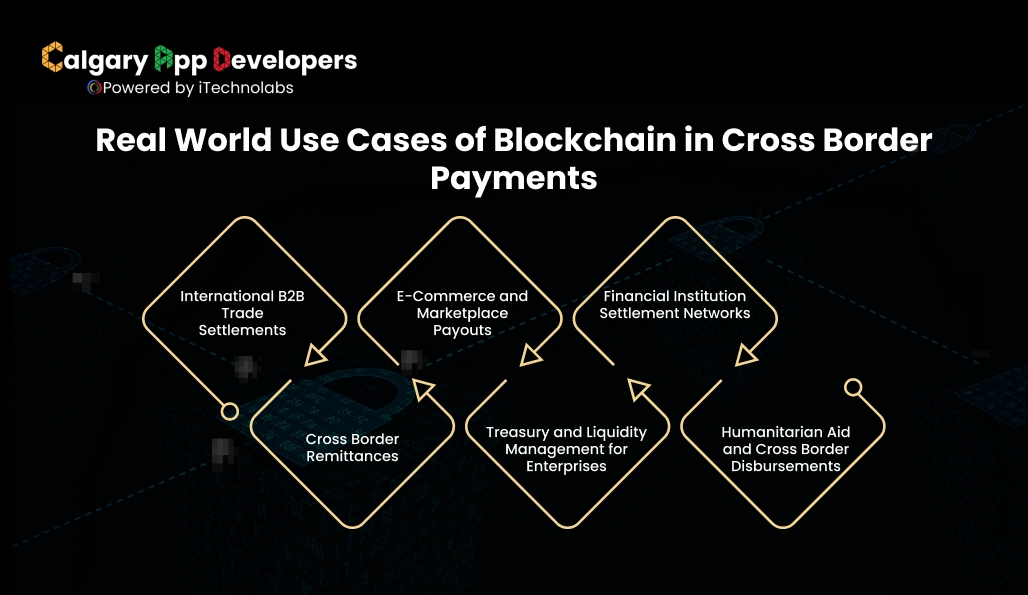

Real World Use Cases of Blockchain in Cross Border Payments

The adoption of blockchain in cross border payments is no longer theoretical. Financial institutions, fintech platforms, and multinational enterprises are deploying blockchain networks to solve specific operational challenges across industries. Below are some of the most impactful real-world use cases.

International B2B Trade Settlements

- Global supply chains depend on timely payments between manufacturers, suppliers, distributors, and logistics providers. Traditional correspondent banking systems often delay settlements by several days, creating cash flow constraints and reconciliation complexity.

- Blockchain networks enable parties to achieve near real-time settlement through their shared access to transparent transaction records. A German manufacturer can use a blockchain-based stablecoin network to pay a raw material supplier in Singapore, which enables funds to settle within minutes while the system records transaction details permanently. The system reduces payment disputes while it decreases foreign exchange expenses and enhancing working capital management.

Cross Border Remittances

- Remittance corridors often involve high transaction fees and slow processing times, especially in emerging markets. Migrant workers sending funds to families frequently pay significant percentages in service charges.

- Blockchain-powered remittance platforms reduce intermediary layers, enabling faster and more affordable transfers. A worker in Canada sending money to India can use a blockchain-based wallet to transfer funds directly to a recipient’s digital wallet or linked bank account. Settlement occurs quickly, and fees are often significantly lower than traditional remittance services.

E-Commerce and Marketplace Payouts

- Global digital marketplaces must process payments to sellers across multiple countries. Delayed settlements and high conversion fees affect seller trust and platform profitability.

- Blockchain in cross border payments allows platforms to automate payouts through smart contracts. For instance, a US based e commerce marketplace can release payments to a seller in Brazil immediately after delivery confirmation, using tokenized fiat or stablecoins. Automated verification and instant settlement improve seller satisfaction and reduce operational overhead.

Treasury and Liquidity Management for Enterprises

- Multinational corporations often maintain multiple pre-funded accounts across different regions to manage cross border obligations. This approach ties up capital and complicates liquidity planning.

- Blockchain-based payment infrastructure enables on-demand liquidity, reducing the need for prefunding. A global technology company operating in Asia, Europe, and North America can settle internal transfers or supplier payments through a blockchain network without maintaining large idle balances in foreign accounts.

Financial Institution Settlement Networks

- Banks are increasingly exploring blockchain consortia to modernize cross border settlement processes. Instead of relying on traditional SWIFT messaging and correspondent relationships, participating institutions share a distributed ledger for faster reconciliation.

- For example, banks in a regional payment corridor can form a blockchain network to settle transactions directly, reducing processing time from days to hours while maintaining regulatory compliance.

Humanitarian Aid and Cross Border Disbursements

- International aid organizations often struggle with transparency and distribution efficiency when transferring funds across borders. Tracking how funds are used can be difficult in complex environments.

- Blockchain provides an auditable transaction trail, ensuring that disbursements reach intended recipients. Aid agencies can distribute digital funds to beneficiaries in crisis regions, with each transaction securely recorded and traceable.

These use cases demonstrate that blockchain in cross border payments is addressing long-standing inefficiencies across trade, remittances, digital commerce, and institutional finance. As infrastructure matures and regulatory clarity improves, adoption across industries is expected to accelerate.

Read Also: What is MPC Wallet? Brief Guide to Multi-Party Computation

Step-by-Step Guide to Building a Profitable Blockchain-Powered Payment Platform

Developing a commercially successful solution powered by blockchain in cross border payments requires more than deploying distributed ledger technology. It demands a strategic blend of regulatory alignment, technical precision, liquidity planning, and long-term scalability. A structured roadmap reduces risk, accelerates time to market, and ensures the platform delivers measurable business value from day one.

Below is a comprehensive step-by-step framework to guide development and commercialization.

Step 1: Define a Focused Market Strategy and Revenue Model

- Identify the primary target segment, such as B2B trade settlements, remittances, marketplace payouts, or institutional transfers.

- Select high-volume corridors with strong transaction demand and regulatory clarity.

- Define revenue streams, including transaction fees, FX spreads, subscription tiers, liquidity provisioning, and API licensing.

- Establish competitive pricing benchmarks against traditional cross border providers.

- Develop a phased rollout strategy to validate product market fit before large-scale expansion.

Step 2: Select the Right Blockchain Infrastructure

- Evaluate public, private, and consortium blockchain models based on governance and compliance requirements.

- Analyze transaction throughput, confirmation speed, and cost predictability.

- Ensure interoperability with core banking systems and payment networks.

- Choose networks that support stablecoins or tokenized fiat for smoother settlement.

- Architect infrastructure capable of scaling with increasing transaction volumes.

Step 3: Embed Regulatory Compliance from the Start

- Integrate digital KYC systems for secure onboarding.

- Implement AML monitoring and automated transaction screening.

- Incorporate sanctions list verification and risk scoring engines.

- Align data storage and reporting processes with jurisdiction-specific regulations.

- Obtain required licenses or collaborate with regulated financial institutions.

Step 4: Build Core Payment and Liquidity Infrastructure

- Develop secure multi-currency digital wallets with strong encryption standards.

- Integrate stablecoins or tokenized assets for efficient settlement.

- Design an intelligent payment routing engine to optimize transaction paths.

- Implement real-time settlement modules for faster fund transfers.

- Deploy smart contracts to automate conditional releases and reconciliation workflows.

- Enable fiat on-ramp and off-ramp functionality for local currency conversion.

- Integrate liquidity management tools to reduce idle capital across jurisdictions.

Step 5: Establish Strategic Partnerships

- Partner with banks for regulated fiat processing and custody services.

- Collaborate with liquidity providers to ensure competitive FX rates.

- Work with custodians for secure digital asset storage.

- Integrate third-party payment processors to expand market reach.

- Build regional alliances to accelerate entry into new cross border corridors.

Step 6: Secure, Test, and Scale

- Conduct comprehensive smart contract audits and security reviews.

- Perform penetration testing to identify and resolve vulnerabilities.

- Stress test the infrastructure under high transaction volumes.

- Continuously monitor transaction performance, costs, and settlement times.

- Expand gradually into additional markets once operational stability is proven.

A disciplined execution of these steps positions organizations to build scalable and profitable infrastructure around blockchain in cross border payments. When technology, compliance, and commercial strategy are aligned from the beginning, the platform evolves from a payment solution into a long-term financial ecosystem capable of supporting global growth.

Also Read: How Much Does It Cost to Build a Cryptocurrency Exchange App like Coinbase?

Technology Stack and Infrastructure Considerations

Building scalable systems for blockchain in cross border payments requires a carefully selected technology stack. Every layer of the infrastructure must support speed, security, regulatory compliance, and future growth. Below is a practical overview of the core components involved.

| Layer | Technology Components | Purpose in Cross Border Payments |

| Blockchain Network | Public blockchains, private blockchains, consortium networks | Enables decentralized settlement, transaction validation, and immutable records |

| Smart Contract Layer | Solidity, Rust, Move, WebAssembly-based contracts | Automates payment execution, conditional settlements, escrow, and reconciliation |

| Digital Assets | Stablecoins, tokenized fiat, CBDC integrations | Supports low volatility settlement and efficient currency conversion |

| Wallet Infrastructure | Custodial wallets, non-custodial wallets, MPC-based wallets | Manages secure storage, signing, and transfer of digital assets |

| Payment Routing Engine | Custom transaction routers, liquidity aggregation logic | Optimizes transaction paths for speed, cost, and liquidity availability |

| Fiat On Ramp and Off Ramp | Banking APIs, payment gateways, settlement partners | Enables conversion between digital assets and local fiat currencies |

| Compliance and Risk Layer | KYC providers, AML engines, and sanctions screening tools | Ensures regulatory compliance across jurisdictions |

| Security Framework | Encryption, key management systems, multi-signature authentication | Protects assets, identities, and transaction integrity |

| API and Integration Layer | REST APIs, GraphQL, webhook services | Connects blockchain systems with banks, ERPs, and enterprise platforms |

| Monitoring and Analytics | Transaction monitoring, audit logs, performance dashboards | Provides visibility into payment status, system health, and compliance reporting |

| Scalability and Infrastructure | Cloud platforms, containerization, and load balancing | Supports high availability, global performance, and horizontal scaling |

A well-designed stack ensures that blockchain in cross border payments operates as enterprise-grade infrastructure rather than experimental technology. The right combination of blockchain networks, compliance tooling, liquidity mechanisms, and scalable infrastructure creates a foundation that can support high transaction volumes, regulatory scrutiny, and long-term business growth.

Addressing Early Stage Risks and Operational Challenges

Adopting blockchain in cross border payments offers measurable advantages, but early-stage implementation comes with operational and strategic risks. Addressing these challenges at the planning stage reduces regulatory exposure, technical setbacks, and financial loss.

- Regulatory Uncertainty Across Jurisdictions

Cross border transactions are subject to varying financial regulations, licensing rules, and reporting standards. Blockchain-based settlement mechanisms may face additional scrutiny related to digital assets and tokenized currencies. Organizations must conduct jurisdiction-specific legal assessments and engage compliance experts before launching into new corridors.

- Liquidity, Volatility, and Asset Stability

When digital assets are used for settlement, volatility can impact transaction value. Even stablecoins carry issuer and reserve risks. Platforms must integrate reliable liquidity providers and implement risk mitigation strategies to ensure predictable settlement outcomes.

- Integration with Legacy Financial Systems

Enterprises and banks operate on established infrastructure. Connecting blockchain networks with core banking systems, payment gateways, and ERP platforms requires secure APIs and standardized data formats. Poor integration planning can delay adoption and disrupt operations.

- Security Vulnerabilities and Smart Contract Risks

Payment platforms are high-value targets for cyber threats. Vulnerabilities in smart contracts, wallet infrastructure, or key management systems can lead to financial losses. Comprehensive security audits and continuous monitoring are essential before scaling operations.

- Scalability and Network Performance Limitations

Public blockchain networks may face congestion during high traffic periods, increasing transaction fees and confirmation times. Selecting the right network architecture and implementing scalability solutions, such as layer two mechanisms, can reduce performance bottlenecks.

- User Education and Trust Barriers

Institutional clients and enterprises may hesitate to adopt blockchain-based systems due to unfamiliarity or perceived risk. Transparent communication, regulatory alignment, and clear audit trails are necessary to build long-term trust.

Successfully managing these early-stage challenges ensures that blockchain in cross border payments evolves from a promising innovation into a stable and commercially reliable financial infrastructure. Proactive risk management strengthens operational resilience and accelerates sustainable adoption across global markets.

Read Also: OTC Crypto Exchange Development: Benefits, Features, Process & Costs

Navigating Global Regulatory and Compliance Requirements

Regulation plays a defining role in the adoption and scalability of blockchain in cross border payments. Because international transactions move across multiple legal systems, compliance cannot be treated as a regional checklist. It must be embedded into product design, operational workflows, and governance structures from the beginning.

United States

In the United States, blockchain-based payment platforms must comply with the Bank Secrecy Act under the oversight of the Financial Crimes Enforcement Network. Most cross border payment providers qualify as Money Services Businesses and must implement strict KYC, AML, and transaction monitoring controls. In addition, state-level money transmitter licenses are often required. The Office of Foreign Assets Control enforces sanctions compliance, particularly for international transfers. Depending on asset structure, oversight may also involve the Securities and Exchange Commission or the Commodity Futures Trading Commission. Stablecoin issuers face increasing scrutiny around reserve backing and disclosure standards.

Canada

In Canada, cross border payment providers dealing in digital assets are regulated by the Financial Transactions and Reports Analysis Centre of Canada. Businesses must register as Money Services Businesses and comply with AML and anti terrorist financing requirements. Provincial securities regulators may assert oversight where digital assets resemble investment products. Compliance with reporting thresholds and identity verification standards is mandatory for international fund transfers.

European Union

The European Union has established a structured framework through the Markets in Crypto Assets regulation, which governs crypto asset service providers. Payment firms must also align with the revised Payment Services Directive and Anti-Money Laundering Directives. The Transfer of Funds Regulation extends travel rule requirements to digital asset transactions, strengthening transparency in cross border transfers.

United Kingdom

In the United Kingdom, the Financial Conduct Authority oversees crypto asset firms under anti-money laundering regulations. Payment service providers must comply with the Payment Services Regulations and Electronic Money Regulations, depending on their structure. Consumer protection and operational resilience requirements are increasingly emphasized.

Asia Pacific

Singapore regulates digital payment token services under the Payment Services Act through the Monetary Authority of Singapore. Japan requires crypto asset service providers to register with the Financial Services Agency. Hong Kong operates under the Securities and Futures Commission licensing regime for virtual asset platforms. India has implemented taxation and reporting rules for digital asset transactions while continuing to refine broader regulatory policy.

Middle East

The United Arab Emirates has introduced structured frameworks through the Virtual Assets Regulatory Authority in Dubai and the Financial Services Regulatory Authority in Abu Dhabi Global Market. These authorities define licensing, capital requirements, and compliance standards for digital asset businesses operating across borders.

Global Compliance Standards

The Financial Action Task Force sets international AML and travel rule guidelines for virtual asset service providers. The Bank for International Settlements and various central banks influence standards for cross border settlement, stablecoin oversight, and central bank digital currency development.

For organizations implementing blockchain in cross border payments, regulatory alignment must extend across onboarding, transaction monitoring, data reporting, and audit mechanisms. Early legal assessment and proactive engagement with regulators significantly reduce expansion risks. As global policies continue to evolve, compliance readiness will remain a foundational pillar for sustainable cross border payment infrastructure.

The Future Outlook of Blockchain in Cross Border Payments

The next phase of global financial infrastructure will be defined by speed, transparency, and programmable value transfer. Blockchain in cross border payments is positioned to move from selective adoption to mainstream financial integration as institutions seek alternatives to slow and capital-intensive correspondent banking networks.

One of the most significant developments will be the expansion of stablecoin-backed settlement systems. As regulatory clarity improves across North America, Europe, and the Asia Pacific, more banks and fintech platforms are expected to integrate regulated digital assets into their payment rails. This shift will reduce dependency on prefunded accounts and improve real-time liquidity management across corridors.

Central bank digital currencies will also influence cross border settlement models. Several central banks are already piloting cross-jurisdiction CBDC interoperability projects. If implemented at scale, these systems could reduce friction between national payment networks while maintaining sovereign control over monetary policy.

Interoperability will become a defining priority. Future payment ecosystems will connect public blockchains, private enterprise networks, and traditional banking systems through standardized APIs and compliance frameworks. Institutions that invest early in interoperable infrastructure will gain a competitive advantage.

Artificial intelligence-driven compliance monitoring, automated FX optimization, and smart contract-based trade finance are expected to further enhance efficiency. Cross border transactions will become increasingly data-driven, secure, and near-instantaneous.

As global trade expands and digital commerce accelerates, blockchain in cross border payments will evolve into a foundational layer of international finance. Organizations that align technology, regulation, and liquidity strategy today will be positioned to lead in a more connected and programmable global economy.

Also Read: How Much Does It Cost to Create Crypto Trading App Like Swyftx?

Final Words

Cross border payments are entering a structural transformation phase. Legacy systems built on correspondent banking relationships are no longer sufficient for a digital economy that demands speed, transparency, and cost efficiency. Businesses operating globally require infrastructure that can support real-time commerce, predictable settlement, and stronger liquidity control.

Blockchain in cross border payments offers a practical path forward. By reducing intermediaries, enabling programmable transactions, and improving traceability, blockchain technology addresses long-standing inefficiencies in international transfers. It also creates new commercial opportunities for banks, fintech firms, and enterprises seeking to modernize their financial operations.

However, success depends on more than technology adoption. Regulatory alignment, secure infrastructure, and strategic liquidity planning are essential to building sustainable solutions. Organizations that approach blockchain with a structured development roadmap and compliance first mindset will gain a measurable competitive advantage.

As global trade volumes rise and digital assets mature, blockchain in cross border payments is set to become a core component of modern financial infrastructure rather than an alternative experiment. The shift has already begun. The question is how strategically businesses choose to participate in it.

FAQs

- What Are Blockchain Based Cross Border Payments?

Blockchain-based cross border payments refer to international fund transfers that are processed and settled using distributed ledger technology instead of traditional correspondent banking networks. Rather than relying on multiple intermediary banks, transactions are validated on a blockchain network and recorded on a shared ledger. This structure improves transparency, reduces settlement time, and lowers transaction costs. In the context of blockchain in cross border payments, digital assets such as stablecoins or tokenized fiat are often used to facilitate faster and more efficient value exchange across jurisdictions.

- How Does Blockchain Technology Enable International Payment Processing?

Blockchain in cross border payments works by using a decentralized network to validate and record transactions in real time. When a payment is initiated, it is broadcast to the blockchain network, verified through a consensus mechanism, and permanently recorded on the ledger. Smart contracts can automate conditional releases of funds, while stablecoins or tokenized currencies help reduce volatility during settlement. Once validated, the transaction reaches finality without the need for multiple correspondent banks, significantly improving speed and traceability.

- How Can Businesses Integrate Blockchain into Their Cross Border Payment Strategy?

Businesses can integrate blockchain in cross border payments by first identifying high-friction corridors or payment flows that suffer from delays and high costs. The next step involves selecting a suitable blockchain infrastructure and partnering with regulated financial institutions for fiat conversion and compliance support. Organizations should embed KYC, AML, and transaction monitoring systems into their architecture. A phased implementation approach, starting with pilot programs, helps validate performance before full-scale deployment across global operations.

- What Are the Key Reasons to Shift Cross Border Payments to Blockchain Infrastructure?

Moving cross border payments to blockchain infrastructure improves settlement speed, enhances transparency, and reduces operational costs. Traditional systems depend on multiple intermediaries, which increases processing time and fees. Blockchain-based systems enable near-real-time transaction validation and immutable record keeping. This strengthens audit readiness and reduces reconciliation errors. For enterprises managing global supply chains or digital marketplaces, blockchain in cross border payments also improves liquidity management and capital efficiency.

- What Risks Should Companies Evaluate Before Adopting Blockchain for Cross Border Payments?

Before implementing blockchain in cross border payments, companies should assess regulatory exposure, digital asset volatility risks, cybersecurity threats, and scalability limitations. Compliance requirements vary across jurisdictions and may impact licensing obligations. Security vulnerabilities in smart contracts or wallet infrastructure can expose platforms to financial loss if not properly audited. Additionally, integration with legacy banking systems requires careful technical planning. A thorough risk assessment combined with legal and technical due diligence ensures sustainable adoption.

Pankaj Arora is a seasoned technology leader and the Founder of Calgary App Developer, with 10+ years of expertise in crafting high-performance digital solutions. His core competencies include full-stack app development, cloud-native architecture, API integration, and agile product delivery. Under his leadership, Calgary App Developers has empowered startups and enterprises alike with scalable mobile applications, secure web platforms, and AI-driven SaaS products.